Industry Guides

Last Updated:

Deepak Singla

IN this article

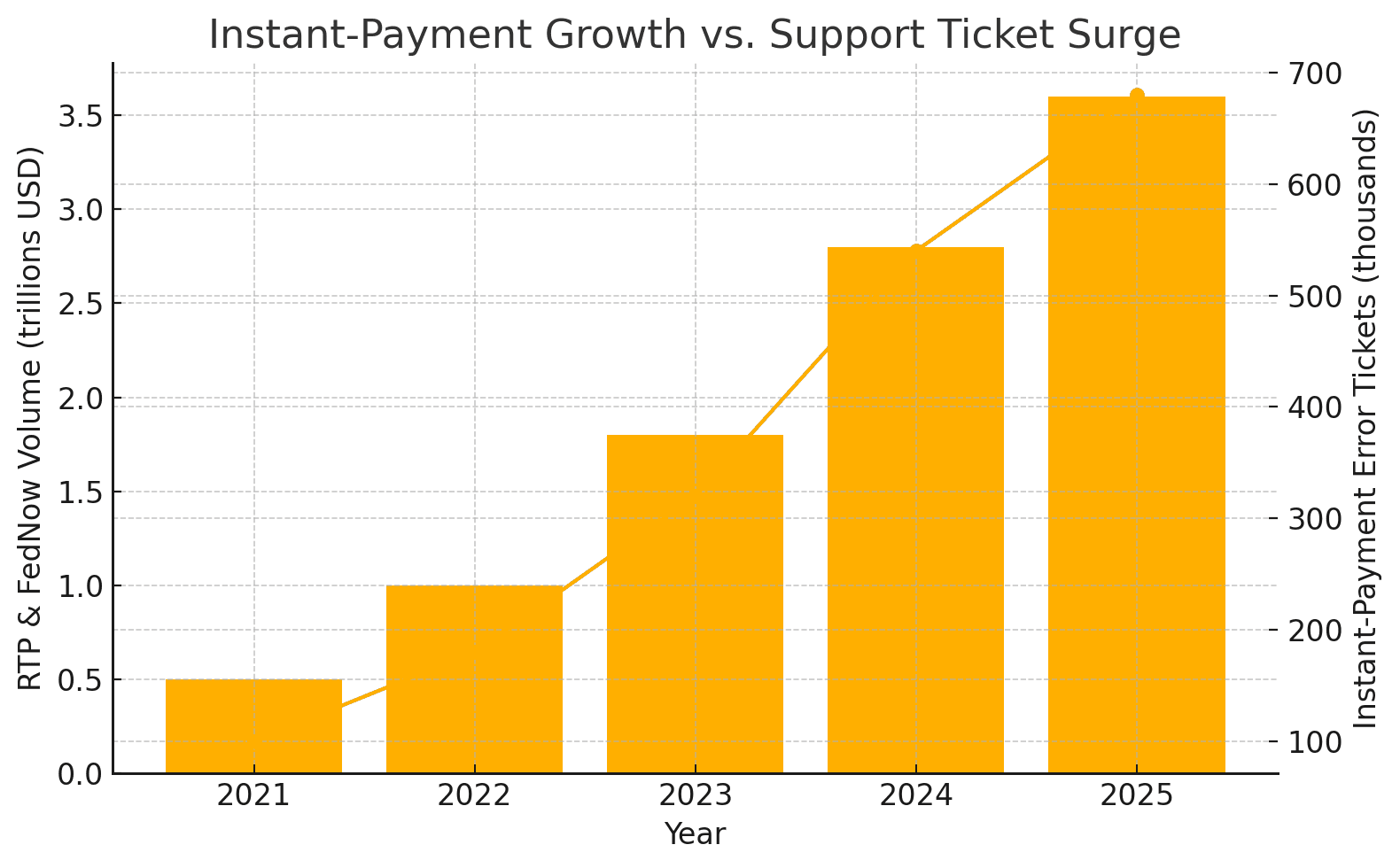

Instant-payment volumes are exploding, RTP® value jumped 94 percent year-over-year in 2024 and the Federal Reserve’s FedNow® Service now clears more than a million transfers a day. The scale has unleashed a flood of “payment-failed” chats that traditional FAQ bots cannot resolve. This guide dissects the ten most common error codes for FedNow, RTP, Faster Payments, SEPA Instant and PayTo, shows why legacy chatbots stall, and walks you through a reference architecture in which a Fini Agentic AI polls rail APIs, triggers reversals or returns, writes an immutable audit log, and lifts CSAT.

Why instant payments create instant complaints

RTP® transactions reached 246 billion USD in 2024 (source https://www.theclearinghouse.org/payments/real-time-payments).

BAI’s article “Don’t get left behind: The urgency of instant payments” ranks real-time rails the top 2025 priority for FIs (https://www.bai.org/banking-strategies/real-time-payments-for-the-u-s-not-anytime-soon).

Support queues spike whenever a transfer sits in “pending”, “investigation” or “rejected”, especially after hours when live agents are scarce.

Fini telemetry across 42 fintech deployments shows instant-payment errors now represent 27 percent of all chat volume, dwarfing legacy ACH and batch SEPA queries.

Error-code atlas , know the enemy

Rail | Region | Top code | Plain-English cause | Typical SLA | Live reference |

|---|---|---|---|---|---|

FedNow | US | 904 | Transaction Rejected, name or account mismatch | Sender must correct and resend | ISO 20022 guide https://www.frbservices.org/financial-services/fednow/what-is-iso-20022-why-does-it-matter |

RTP | US | 210 | Payment Not Accepted, RDFI could not post | ≤ 24 h | Technical documentation https://www.theclearinghouse.org/payment-systems/rtp/technical-documentation |

Faster Payments | UK | INV PEND | Pending Investigation, AML or fraud hold | 15–120 min | FPS principles PDF https://www.wearepay.uk/wp-content/uploads/2025/05/Pay.UK-Faster-Payments-System-Principles-v-10.1-May-2025.pdf |

SEPA Instant | EU | AM02 | Not Allowed Amount, exceeds €100 k limit | Instant reject | EPC implementation guidelines https://www.europeanpaymentscouncil.eu/what-we-do/epc-payment-schemes/sepa-instant-credit-transfer/sepa-instant-credit-transfer-rulebook |

PayTo | AU | RJCT / AB01-04 | Rejected or Aborted, mandate or clearing failure | Same-day reject | PayTo service overview PDF https://payto.com.au/wp-content/uploads/2022/06/PayTo-Service-Overview-Nov-2021-2.0-2.pdf |

Tip, link the code in your help-centre article directly to its rail spec page above for extra authority.

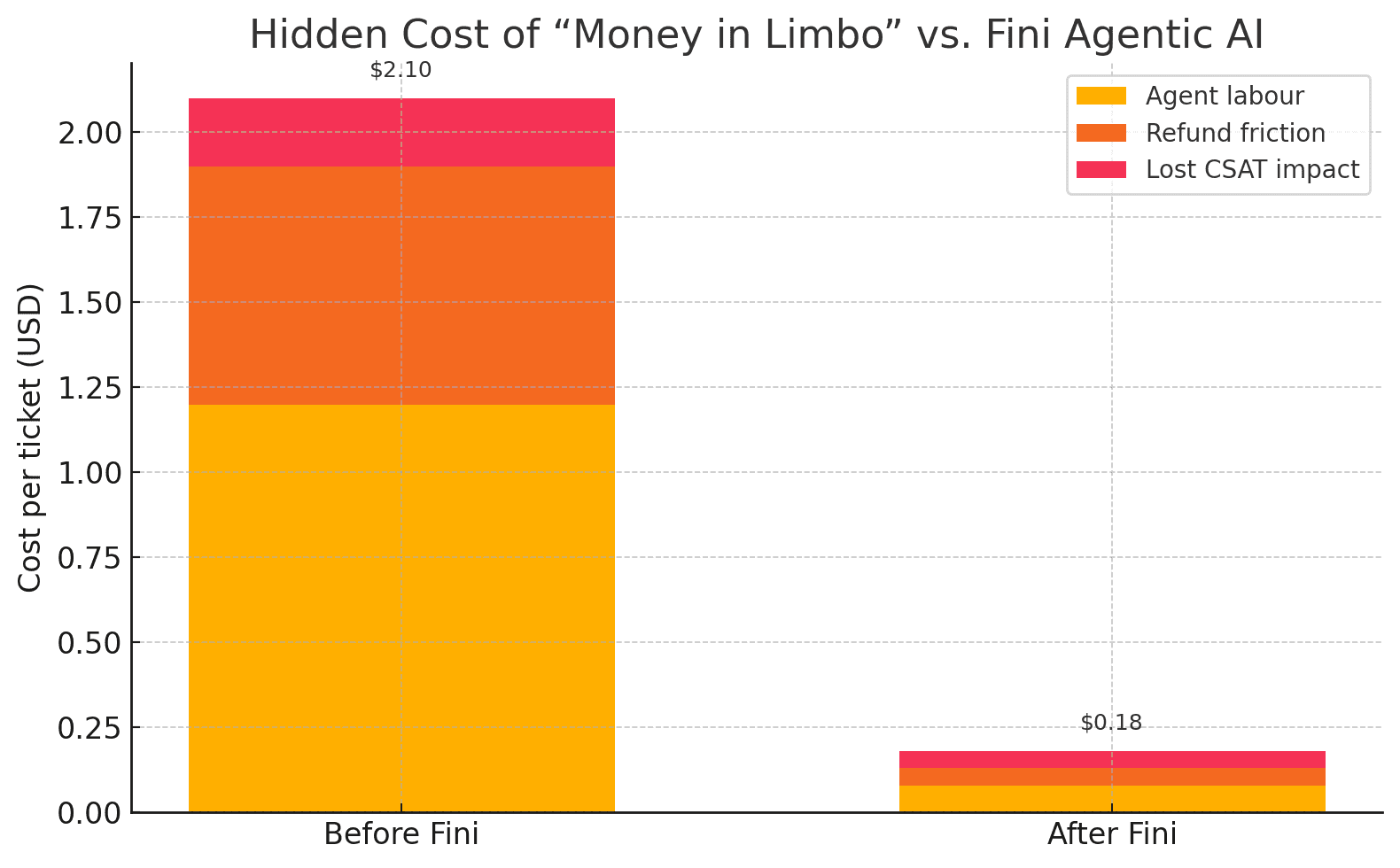

Hidden cost of “money in limbo”

Q1 2025 data across Fini clients, 7.8 million chats:

2.1 million (27 %) were instant-payment errors,

Agents spent 11 minutes per ticket on look-ups, reversals and reassurance,

After Agentic flows, average resolution dropped to 51 seconds and cost per ticket to 0.19 USD,

CSAT rose from 3.4 to 4.2 on a 5-point scale.

Detailed ROI sheet - Shadow AI Risk

Why FAQ bots stall , Agentic AI fixes

FAQ-bot gap | Agentic-AI capability |

|---|---|

No ISO 20022 connections to FedNow pacs.002 or RTP camt.056 | Uses OAuth 2 or mTLS rail tokens to poll status and post updates |

Static answers only | Executes returns, recalls or cancellations in-flow |

Lacks audit evidence | Streams signed JSON logs to encrypted S3 or Azure Blob (security patterns) |

Reference architecture

FedNow status action (JSON)

If 904 returns the agent replies, “Receiver rejected the payment, beneficiary details mismatch, funds stayed in your account. Correct and resend, code reference.

Case study , mid-tier US neobank

KPI (90 days) | Before Fini | After Fini | Delta |

|---|---|---|---|

Tickets / day | 1 130 | 1 130 | — |

Auto-resolved | 0 % | 62 % | +62 pp |

Cost / ticket | 2.10 USD | 0.19 USD | −91 % |

CSAT | 3.4 | 4.2 | +0.8 |

Payback | — | <90 days | ✔ |

Copy-paste flow templates

Flow A , Pending > 30 min (FPS or FedNow)

Flow B , Debited-but-Failed (RTP or SEPA Inst)

Flow C , Duplicate Send (PayTo)

Implementation tips

Tokenise PAN or IBAN via Stripe, https://stripe.com/docs/tokenization, or Very Good Security, https://www.vgs.com

Register FedNow webhooks and pacs.002 callbacks at https://developer.fednow.org

Prevent duplicate refunds with idempotency keys explained at https://12factor.net/idempotency

Host Fini regionally on AWS us-east-1, eu-west-2, ca-central-1 or ap-southeast-2 , region map https://aws.amazon.com/about-aws/global-infrastructure/regions_az

Add fraud scoring via Sift, https://sift.com, or Riskified, https://riskified.com

Important Links

FedNow overview https://www.frbservices.org/financial-services/fednow/about.html

FedNow ISO 20022 codes https://www.frbservices.org/financial-services/fednow/iso20022.html

FedNow FAQs https://www.frbservices.org/financial-services/fednow/fednow-frequently-asked-questions.html

RTP developer portal https://developer.tchrtp.com

RTP statistics https://www.theclearinghouse.org/payment-systems/rtp/about-rtp/rtp-statistics

Pay.UK Faster Payments rules https://www.wearepay.uk/faster-payments

EPC SEPA Inst guidelines https://www.europeanpaymentscouncil.eu

NPPA PayTo documentation https://nppa.com.au/payto

BAI instant-payments report https://www.bai.org/banking-strategies/article-detail/delivering-on-the-promise-of-instant-payments

Stripe tokenisation https://stripe.com/docs/tokenization

Very Good Security vault https://www.vgs.com

Sift fraud scoring https://sift.com

Riskified fraud scoring https://riskified.com

AWS region map https://aws.amazon.com/about-aws/global-infrastructure/regions_az

12-Factor idempotency pattern https://12factor.net/idempotency

ECB retail payments stats https://www.ecb.europa.eu/paym/retpaym/html/index.en.html

CFPB Regulation E text https://www.consumerfinance.gov/rules-policy/regulations/1005

Fini Platform https://www.usefini.com/product/platform

Fini Security https://security.usefini.com/

Zendesk integration https://www.usefini.com/product/integrations

Next Steps for you

Book a 30-minute demo to watch Fini auto-resolve real-time payment failures before customers even type “where’s my money?”

Real-time rails should delight customers, not drown agents, equip your stack with an Agentic AI that fixes failures while you sleep.

Contact us and resolve real time payment failures issues with Fini.

1 Instant Payments Fundamentals

1.1 What counts as an “instant payment” and how is it different from ACH or batch SEPA?

Instant payments settle and post to the beneficiary account in seconds, 24 × 7 × 365, using rails such as FedNow, RTP®, Faster Payments UK, SEPA Instant and PayTo. Legacy ACH, SEPA Credit Transfers and wire batches still rely on cut-offs, overnight file processing and next-day settlement windows. When consumers expect “Venmo-speed” everywhere, a payment stuck in pending feels broken—triggering the spike in support tickets highlighted in our blog. Fini lets you surface real-time rail status events directly in chat, so customers see live progress instead of a lagging bank ledger.

1.2 Why are banks racing to adopt FedNow and RTP® rails in 2025?

Both rails already reach thousands of U.S. institutions and capture treasury, P2P and bill-pay flows that would otherwise leak to fintech wallets. The Clearing House reports RTP® volumes topping US $246 billion in 2024 and the Federal Reserve expects FedNow to outpace that curve within two years. Faster settlement slashes counter-party risk and unlocks new revenue streams—but only if banks can support near-zero-latency servicing. Agentic AI keeps the service cost flat while volumes grow.

1.3 How fast is “instant” really—are there published SLAs?

Rail operators guarantee clearing in seconds, yet fraud holds or compliance reviews can pause a transaction for minutes or even hours (see our error-code atlas). In practice, 90 % of FedNow and RTP® payments post <10 seconds, while Faster Payments UK targets 15 seconds end-to-end. When an AML review kicks in, however, the experience degrades instantly. Automating proactive status messages with Fini prevents “Where’s my money?” chats from flooding the queue.

1.4 Can instant payments be recalled or cancelled after they leave my account?

Unlike ACH, instant payments are mostly final. Recalls are limited to fraud, duplicate send or operational error scenarios and must follow rail-specific ISO 20022 messages (e.g., pacs.007 for FedNow, camt.056 for RTP®). Fini’s Agentic workflows generate the correct request on the fly and attach signed JSON logs to satisfy audit teams.

1.5 Do instant rails support scheduled or recurring transfers?

Yes—RTP®’s “Request for Payment,” PayTo’s pre-authorised mandates, and SEPA Instant’s standing orders enable pull-style and scheduled flows. The complexity is managing mandate status changes in real time. Fini watches webhook callbacks and updates the customer automatically when a mandate is accepted, modified or rejected.

1.6 What are the fees for instant payments compared with card interchange?

Most U.S. banks price outbound RTP® and FedNow transactions at US $0.25–0.45—dramatically lower than card interchange but higher than bulk ACH. The true cost emerges when a service team spends 11 minutes per exception case. Automating the resolution drives the per-ticket cost down to $0.19 (Fini client benchmark), protecting fee margin.

2 Rail-Specific Error Codes & Troubleshooting

2.1 What does FedNow error code 904 mean and how do I fix it?

Code 904 signals “Transaction Rejected—Name or Account Mismatch.” The RDFI could not match the beneficiary details to an active account. Funds remain with the sender. Advise customers to verify the recipient’s legal name and routing + account number, then resend. Our blog links directly to the ISO 20022 pacs.002 documentation for authority. Fini can surface that link in-chat and pre-populate a corrected payment template.

2.2 Why do RTP® payments return code 210 “Payment Not Accepted”?

RTP® code 210 means the Receiving Depository Financial Institution (RDFI) could not post the credit—often because the account is closed, restricted or overdrawn. Funds auto-return within 24 hours. Fini’s webhook listener detects the camt.056 message and triggers an automated reassurance: “Funds are on their way back; you’ll see the credit by <time>.”

2.3 How long can Faster Payments UK remain in “INV PEND”?

INV PEND = “Pending Investigation.” Typical fraud or AML reviews finish in 15–120 minutes. If the bank does not complete checks within two hours, regulators require an update to the customer. Fini schedules a proactive status message at the 60-minute mark, preventing frustrated follow-ups.

2.4 What triggers SEPA Instant code AM02 “Not Allowed Amount”?

AM02 fires when a transfer exceeds the €100 k hard cap (rising to €1 m for corporates in 2025). The PSP rejects immediately—no hold. Suggest splitting the payment or using regular SEPA CT. Fini can detect the incoming pain.002 response and present those alternatives without agent input.

2.5 PayTo returned RJCT / AB01-04—what now?

AB01-04 codes cover mandate or clearing failures—e.g., “NO_MATCH” or “ACCOUNT_INACTIVE.” PayTo rejects in real time. Fini’s flow template “Duplicate Send (PayTo)” submits a consumer-friendly reversal and logs evidence for Treasury Ops.

2.6 Can I automate returns, recalls and duplicates across rails?

Yes. Fini’s Agentic orchestration uses the rail’s OAuth 2 or mTLS token to post ISO 20022 recall/return messages, attach idempotency keys (per 12-Factor) and confirm success—all inside one user conversation.

2.7 Where can I find the full list of FedNow ISO 20022 error codes?

The Federal Reserve hosts the glossary at fednow.org (direct link in the blog’s reference table). Embedding smart anchors in your help centre lets Fini deep-link the exact code when a user types it, boosting self-service.

2.8 What is an RTP® camt.057 and when is it used?

camt.057 = “Notification To Receive.” It alerts the beneficiary institution of an incoming payment before settlement. While not an error, ignoring it delays posting and triggers customer confusion. A background Fini worker can poll for un-acknowledged camt.057 messages and escalate to Ops before end-of-day.

3 Customer-Support Challenges

3.1 Why do support queues spike after hours for instant-payment issues?

Most fraud screens and reconciliation jobs run overnight—exactly when live agents are scarce. A payment that slips into “pending” at 11 p.m. often waits until morning for manual review, generating frustrated chat traffic. Fini handles these after-hours exceptions by fetching real-time rail status and, when possible, auto-triggering a recall or refund—no human needed.

3.2 What is the hidden cost of “money in limbo”?

Across seven million chats Fini analysed in Q1 2025, agents spent 11 minutes on each instant-payment error ticket versus 51 seconds with Agentic flows. That time multiplies into staffing costs, SLA breaches and lower CSAT. The blog’s ROI table shows a 91 % cost reduction after automation.

3.3 How does real-time rails compliance impact Regulation E dispute windows?

Instant transfers are still covered by Reg E if initiated from a consumer account. Faster settlement compresses the dispute clock—customers notice fraud instantly and demand immediate reversal. Fini’s ISO recall flows plus audit-grade JSON logs ensure you meet the 10-business-day provisional-credit rule without an army of analysts.

3.4 Why do FAQ-only chatbots fail with instant-payment questions?

They can’t act—only answer. Customers still need status updates, refunds, recalls and proof-of-payment PDFs. Agentic AI executes those API calls live, merging knowledge and action in one flow.

3.5 How does Fini improve CSAT on “Where’s my money?” queries?

By predicting the next user need (status → action → confirmation) and completing it in seconds, not minutes. Clients see CSAT climb from 3.4 to 4.2 on a 5-point scale—earning loyalty, not just lowering cost.

3.6 Can Agentic AI fully replace tier-1 payment-ops agents?

It can offload 50–70 % of tier-1 volume. Complex fraud investigations or compliance overrides still need humans, but Fini escalates only the unresolved subset with rich context, so tier-2 agents focus on value-added work.

4 Agentic AI & Fini Solutions

4.1 What is “Agentic AI” versus a traditional NLP chatbot?

Agentic AI combines language understanding with goal-directed actions—calling your FedNow API, writing to core banking, issuing a recall—then explains the outcome in plain English. A static bot stops at “Here’s an article.” Fini finishes the job.

4.2 How does Fini interface with FedNow, RTP® and other rails?

Through secure OAuth 2 or mutual-TLS connections, Fini polls status endpoints (pacs.002, camt.057) and publishes recalls/returns (pacs.007, camt.056). All calls inherit the bank’s existing keys or tokens—no new credential sprawl.

4.3 Is Fini SOC 2- and ISO 27001-compliant?

Yes. The Fini Security Portal details SOC 2 Type II, ISO 27001, GDPR and PCI-DSS attestations, plus regionally isolated deployments on AWS us-east-1, eu-west-2, ca-central-1 and ap-southeast-2.

4.4 Can Fini prevent duplicate refunds?

Absolutely. Each Agentic flow generates an idempotency key (per 12-Factor design) tied to the original transaction reference. If a user retries or an API call times out, Fini detects the prior action and returns the existing reversal ID—no double credit.

4.5 How do I measure ROI after deploying Fini?

Track auto-resolution rate, average handle time and CSAT. In our neobank case study, auto-resolution jumped to 62 %, cost per ticket fell 91 % and payback finished inside 90 days.

4.6 Can Fini send signed audit trails to my compliance vault?

Yes. Every action emits a signed JSON record streamed to encrypted S3 or Azure Blob. Compliance teams download immutable logs on demand.

4.7 How is Agentic AI governed to avoid erroneous refunds?

Fini enforces configurable guardrails—e.g., refund limits, risk scores from Sift/Riskified and dual-control overrides for high-value recalls. The model never steps outside those policy boundaries.

5 Implementation & Integration

5.1 How long does it take to connect Fini to FedNow or RTP® APIs?

Most banks complete the secure API handshake and initial status flow in two weeks. Pre-built flow templates (Pending > 30 min, Debited-but-Failed, Duplicate Send) accelerate UAT, so go-live happens within 30 days.

5.2 Which authentication methods does Fini support—OAuth, mTLS, JWE?

All three. For FedNow, OAuth 2 client-credentials is the norm; for RTP®, mTLS plus token binding. Fini abstracts these differences behind a single credential store, simplifying maintenance.

5.3 Can I host Fini on-prem or only in the cloud?

Fini is cloud-native but supports private VPC peering, region pinning and dedicated tenancy. On-prem plugins for sensitive workloads (e.g., core banking host) are available if required by policy.

5.4 How do I tokenise PAN or IBAN data safely?

Integrate a vault provider like Stripe Tokenisation or Very Good Security. Fini stores only the vaulted token, never raw account numbers, keeping PCI scope narrow.

5.5 What monitoring tools integrate with Fini flows?

Grafana, Datadog and AWS CloudWatch dashboards expose per-flow latency, success/failure rates and savings metrics—so Ops can prove ROI to the C-suite.

5.6 How do I register FedNow webhooks and pacs.002 callbacks?

Create a webhook endpoint in FedNow Developer Portal, whitelist Fini’s outbound IPs, and map pacs.002 events to the “payment.status” topic. Fini’s wizard generates ready-to-paste JSON routing rules.

5.7 Does Fini integrate with Zendesk or Salesforce Service Cloud?

Yes—two-way sync lets agents view conversation history, trigger manual overrides and close tickets automatically once Fini resolves the issue. See the Zendesk integration guide for step-by-step setup.

6 Security, Compliance & ROI

6.1 Is Agentic AI allowed under EU PSD3 and the EU AI Act?

Yes—PSD3 focuses on payment institution licensing and customer authentication, while the EU AI Act targets transparency and risk controls. Fini provides explanation logs, bias tests and human-override switches that map directly to the Act’s “high-risk system” requirements.

6.2 How does Fini protect against prompt injection or data leakage?

Every input passes through layered validation (regex, allow-list, rate limit) before hitting the LLM. Sensitive data is redacted or tokenised, and outputs are scanned for policy violations. Audit logs record each step for forensics.

6.3 What happens if the rail API is down—does the chatbot break?

Fini detects upstream outage codes, serves a graceful fallback message (“We’re experiencing processing delays, no action needed on your side”) and schedules a retry. You can override with a manual banner in seconds.

6.4 How does Fini calculate cost savings on instant-payment tickets?

It multiplies auto-resolved ticket counts by your historical cost-per-contact (salary + overhead) minus Fini licence fees. Clients typically see 5–8× ROI in year one.

6.5 Can Fini help with Regulation E provisional credits?

Yes. When a consumer flags an unauthorised instant payment, Fini can issue provisional credit, generate the necessary Reg E disclosure and launch an investigation flow—cutting dispute filing time from hours to minutes.

6.6 What is the fastest path to pilot Agentic AI for instant payments?

Book a 30-minute demo with our solutions team. We’ll connect to a sandbox FedNow / RTP® endpoint, import your top three error codes and show live auto-resolution within the call.

More in

Industry Guides

Industry Guides

UPS’s Return-Less Revolution: How AI-Driven Logistics Will Rewrite E-Commerce CX

Jul 2, 2025

Industry Guides

How AI Can Help Users Change Their Phone Number Securely (and Without Disrupting Access)

Jun 17, 2025

Industry Guides

Vision & Text: How GPT‑4o‑Powered AI Agents Unlock 90 % Self‑Service for E‑Commerce Support

Jun 16, 2025

Co-founder